The Growth “Badlands”: When More Sales Produce Less Profit

Business owners naturally assume that more sales will produce more profit. Often, they do. But growth does not always occur in a smooth, predictable line — and the gap between new overhead and new revenue can quietly drain cash even as the business appears to be thriving.

There are points at which a company must increase its overhead before it has enough additional revenue to support that overhead. The business may hire another manager, expand into a larger building, purchase equipment, adopt new software, add administrative personnel, or establish another location. These investments may be necessary for future growth, but they begin costing money immediately.

The expected revenue may take months — or even years — to fully develop.

We refer to this difficult transition period as the growth “badlands.” It is the point where the business has outgrown its old operating structure but has not yet generated enough additional gross profit to support the new one. During this period, sales can increase while profits decline and cash becomes tighter.

Growth Happens in Steps, Not Straight Lines

A small business can often operate efficiently for a period of time using its existing people, equipment, and facilities. As sales increase, the business may initially produce additional revenue without adding significant fixed costs. Because the existing overhead is already being paid, much of the additional gross profit can flow to the bottom line.

Eventually, however, the company reaches a capacity limit. Employees become overloaded. Customer service begins to suffer. Billing is delayed. Projects take longer to complete. The owner becomes involved in too many operational details. To continue growing, the business must make another investment in capacity — and that investment creates a step-up in overhead.

For example, the company may need to add:

- A manager or supervisor

- Administrative and accounting personnel

- Additional production employees

- A larger office, warehouse, or facility

- Vehicles, machinery, or equipment

- More sophisticated software and technology

- Additional insurance, licensing, or compliance support

- A new location or service department

These costs may be necessary and ultimately profitable. However, they are generally incurred before the new capacity is fully utilized. That timing difference creates the growth badlands.

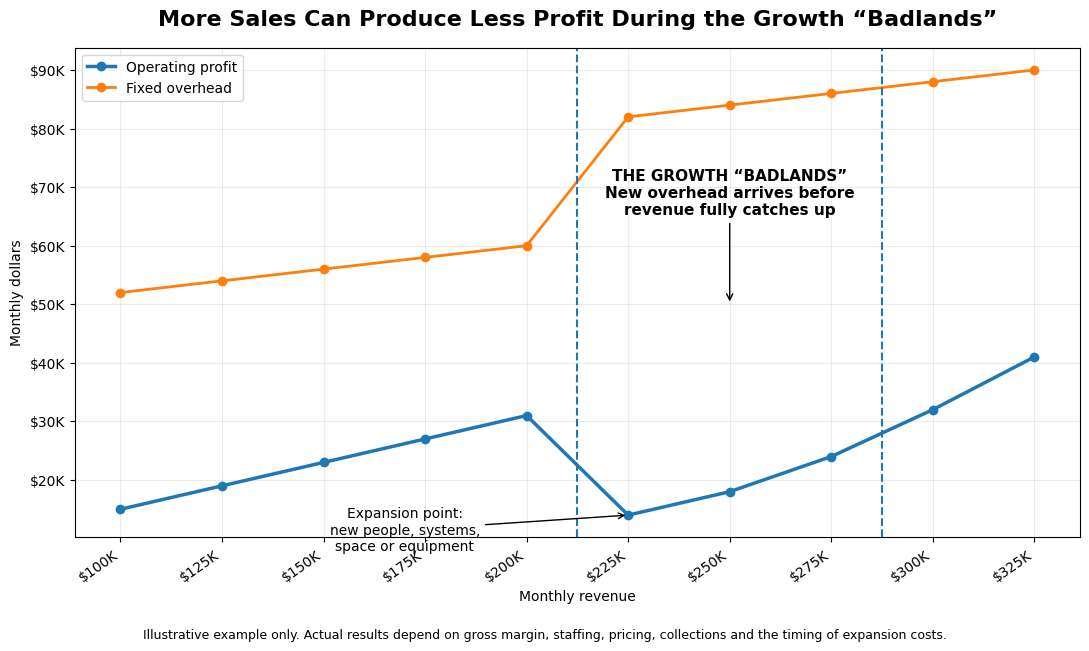

The Chart: How More Revenue Can Temporarily Produce Less Profit

In the example, monthly revenue grows from $100,000 to $200,000, and operating profit increases from approximately $15,000 to $31,000. At that point, the company reaches its operating capacity.

To continue growing, it adds personnel, systems, space, or equipment. Monthly fixed overhead increases from approximately $60,000 to $82,000. Revenue then increases from $200,000 to $225,000 — but operating profit falls from approximately $31,000 to $14,000.

$31K

Profit at $200K revenue

$14K

Profit at $225K revenue

$300K

Revenue to recover profit

The company is producing more sales, serving more customers, and doing more work — but it is making less money. The area between the expansion point and the recovery of profitability is the growth badlands. This does not necessarily mean the expansion was a mistake. It means the business must have enough capital, cash flow, and management discipline to survive the transition.

Why the Growth Badlands Can Be Dangerous

The growth badlands can be difficult to recognize because many traditional signs appear positive. Sales are increasing. The business is hiring. The company may have more customers, more equipment, and a larger market presence. From the outside, the business appears successful. Internally, however, several financial problems may be developing.

The owner may respond by pushing for even more sales. But additional sales do not automatically solve the problem — especially when the new work has weak margins, requires additional working capital, or creates more operational stress. In some cases, aggressively pursuing revenue without understanding the related costs can push the business deeper into the badlands.

Gross Profit Matters More Than Sales

The company does not escape the growth badlands merely by increasing revenue. It escapes when it generates enough additional gross profit to cover the new overhead. This distinction is critical.

Illustrative example: $100,000 of new fixed overhead

At 40% gross margin

$250,000

additional revenue needed

$100,000 ÷ 40% = $250,000

At 25% gross margin

$400,000

additional revenue needed

$100,000 ÷ 25% = $400,000

That additional revenue would only restore the company to its prior profit level — it would not create any additional return on the investment or compensate the owner for the added risk.

This is why revenue targets should not be developed without also considering margins. A lower-margin customer, contract, or product may generate significant activity without producing enough gross profit to support the company's expanding cost structure.

Common Ways Businesses Enter the Badlands

Hiring Ahead of Revenue

New employees begin receiving paychecks immediately, but it may take time for them to become fully productive. There may also be recruiting costs, training time, payroll taxes, employee benefits, computers, vehicles, uniforms, software licenses, and management time. The true cost of adding an employee is substantially more than the base salary.

Expanding Facilities

A larger facility may require increased rent, utilities, insurance, security, maintenance, furnishings, and equipment. The business may also experience moving costs and operational disruption before receiving any benefit from the expansion.

Opening Another Location

A second location can duplicate expenses that were previously shared — another manager, receptionist, lease, utility account, technology system, inventory supply, and marketing budget. Revenue at the new location may develop much more slowly than anticipated.

Adding Management

Hiring a qualified manager can be one of the best investments a growing company makes. However, management salaries are generally fixed costs. The company must produce enough additional gross profit to support the position.

Purchasing Equipment

Equipment may increase capacity, but it can also create loan payments, insurance costs, repairs, maintenance, training expenses, and downtime. The financial analysis should consider all of these costs — not just the purchase price.

Warning Signs That the Business Is in the Badlands

Business owners should pay attention when:

- Revenue is increasing but net income is declining

- Payroll is increasing faster than gross profit

- The company is busier but has less cash

- Accounts receivable are growing faster than sales

- The line of credit is not being paid down after customers pay

- Owner distributions are being funded with borrowed money

- New employees or equipment are not producing the expected capacity

- The business cannot clearly identify its break-even revenue

- Management is relying on future sales to pay current bills

- Financial statements are not being reviewed frequently enough to identify the problem

These warning signs do not always mean the company should stop growing. They mean growth should be managed intentionally.

How to Cross the Growth Badlands Safely

Calculate the New Break-Even Point

Before adding fixed overhead, determine how much additional gross profit — and therefore how much additional revenue — will be required. The calculation should include the full cost of the expansion, not merely the most visible expense.

Prepare a Cash-Flow Forecast

Profitability alone does not determine whether the business can fund its growth. Prepare a rolling cash-flow projection that includes customer collections, payroll, taxes, debt payments, capital purchases, vendor payments, and owner distributions. The forecast should identify when cash is expected to become tight and how the shortage will be funded.

Establish Adequate Cash Reserves

The business should not assume that the new revenue will arrive immediately. Hiring may take longer than expected. Employees may require more training. Customers may delay decisions. Construction or equipment installation may be postponed. Receivables may be collected more slowly. Cash reserves provide time for the new capacity to begin producing results.

Track Results Separately

Whenever possible, track the financial performance of the new employee, department, location, service line, or equipment separately. Without this information, an unsuccessful expansion can continue consuming cash without receiving appropriate attention.

Protect Pricing and Margins

A company should not attempt to escape the badlands by accepting any available work. Discounted or poorly priced work may increase revenue while extending the period of weak profitability. Management should understand the gross profit produced by each major customer, project, product, and service line.

Use Milestones Instead of Assumptions

Before approving the next phase of expansion, establish measurable milestones — such as minimum customer counts, gross profit targets, utilization levels, or cash reserve floors. These milestones allow management to respond to actual results instead of continuing to invest based on optimism.

Growth Is Not the Same as Financial Success

A larger business is not automatically a better business. Growth should eventually produce stronger cash flow, sustainable profits, an improved balance sheet, and an appropriate return for the owners. If additional revenue continually requires more debt, more owner investment, and more financial stress, the underlying business model should be examined.

The growth badlands are not always avoidable. Many successful companies must cross them as they develop the people, systems, and infrastructure necessary to reach the next level. The key is recognizing the badlands before entering them.

Planning a major hire, equipment purchase, or new location?

At Barranco & Associates, we help business owners evaluate the financial impact of expansion, calculate break-even targets, develop cash-flow projections, and monitor whether growth investments are producing the expected results. Before making the next major move, determine how deep the growth badlands may be — and whether the company has the financial resources to cross them.

Talk Through Your SituationCategories

Published

July 13, 2026

Key Insight

At a 25% gross margin, adding $100K of overhead requires $400,000 of additional revenue just to break even — before any additional profit.